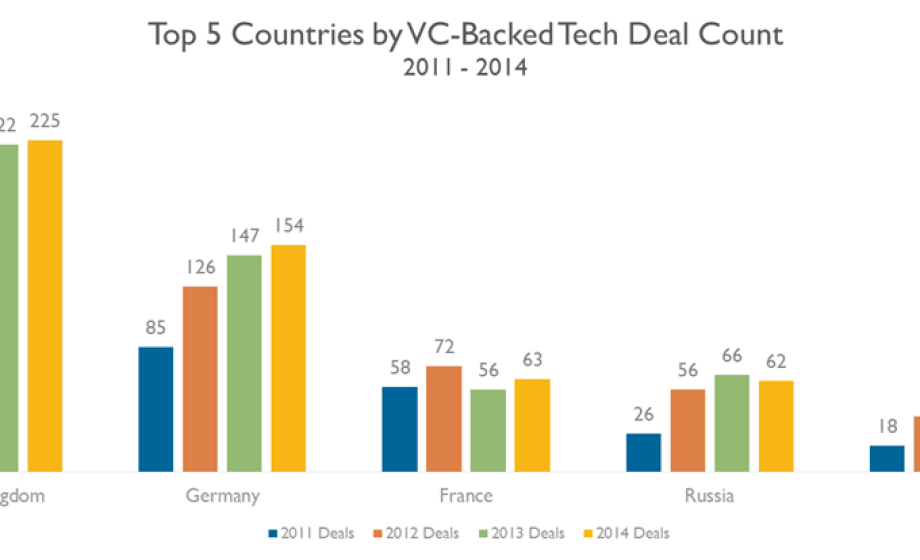

Last week CBInsights published a report on aggregate VC deal volume in the top five European geographies over the past four years. I encourage you to experiment with a free trial of the service for the underlying data, but here’s the headline graphic:

This chart triggered some predictable wailing and gnashing of teeth in France, as the data indicates an indisputable trend that both the UK and Germany are pulling away from France in tech startup financings. It seems not that long ago that the French rooster crowed about its leadership position ‘on the continent’ in VC investment activity. Perhaps more painful yet, both Russia and Spain, while trailing France in total VC deal count, demonstrate impressive growth — 34% and 39% annualized average growth over the period — whereas France is essentially flat at under 3% annually.

Let me first offer a few observations about some interpretations of this data:

- First, there is no evidence of a direct causation between VC investment activity and the rise of successful global tech startups. The mere existence of a lot of VC money sloshing around in a given market does not necessarily mean that more high-quality projects are being financed. Sometimes the converse is actually the case. For example, when excessive tax rebate money flooded the French market, it enabled the subsistence of a troop of zombie startups hovering on the verge of death but somehow hanging on thanks to clever scrapping for subsidies or their drip-feeder VCs, adversely shackling up talent and depriving it from the daylight of other potentially innovative projects.

- Secondly, charts like this one, and rankings in general, are a trick to grab headlines. Let me play with the axes, and I can make a week-dead blobfish look charming.

- Thirdly, from any nation that appears on the disadvantaged end of a statistical report, one of two predictable reactions are elicited: i) victimization (e.g. the Anglo-saxon press dislikes our country, or ii) excuse-making (e.g. “yes, but this data ignored the strong social pact of our country which does not place capitalization above all else…” or “yes, but we have different time horizons in our country and hence a unique measure of success is needed for us.”)

Coming back to potential insights we could glean from this data…

Although there is not a direct causation, there is, however, a correlation between abundant equity financing and the odds for success of startups in a given market. Insufficient risk capital limits a startup’s growth potential. More capital usually translates into more deals, not categorically good deals, but nonetheless the generation of momentum and buzz around entrepreneurship. This is generally a positive development for many European countries whose celebration of entrepreneurship (and the corresponding notion of failure) is still nascent.

Today, the French VC sector represents a market in flux: shifting from tax-incentivized retail vehicles into professional independent funds with sophisticated LPs as investors. This shift is healthy, I would argue, and yet is not reflected in this chart. As this evolution manifests itself over the next few years, it will be interesting to revise this deal count chart at that point.

Furthermore, an overlay charting the future outcomes of the companies backed by VCs in this original chart will be an interesting analysis within 5 to 10 years. Call it a ‘where are they now?’ exercise.

For France: let’s not get our panties in a bunch about this report. Dismissing or counter-arguing it is simply a variation of celebrating mediocrity. Let’s not lose sight of the ultimate objective: building businesses with the ability to succeed on a global scale.

Finally, here’s a radical idea: why don’t we Europeans consider becoming a bit more country-agnostic?

None of our domestic markets are sufficiently massive to justify not looking internationally. When the New York Times squawks about how “Venture capital has been pouring into Europe’s tech scene, with the continent’s start-ups beginning to regularly draw growth funding rounds of $10m or more,” we should feel proud as Europeans that our continent’s tech sector is increasing in vibrancy, whether we be French, English, German… even Scottish.